GAS, BETWEEN ENERGY TRANSITION AND ASPECTS OF GEOPOLITICS

by Jonathan García Gaitan - Director Gas Operations

The recent attack on two oil tankers in the Strait of Hormuz – the strip of land that divides the Arabian Peninsula from Iran – has alarmed the world not only for the possible political repercussions (in relations between the US, Iran and the Gulf countries) but also for the consequences on the trade of hydrocarbons. Specifically, there were fears of an increase in the price of LNG (liquefied natural gas) that passes through the Strait in large quantities, transported by ships from Qatar. In the event of political turbulence, a sharp increase in prices is likely, as suggested by the diplomatic skirmishes between the United States and Iran in recent weeks. The most serious consequences will be suffered by those importing nations that are not very independent from an energy point of view, including Italy.

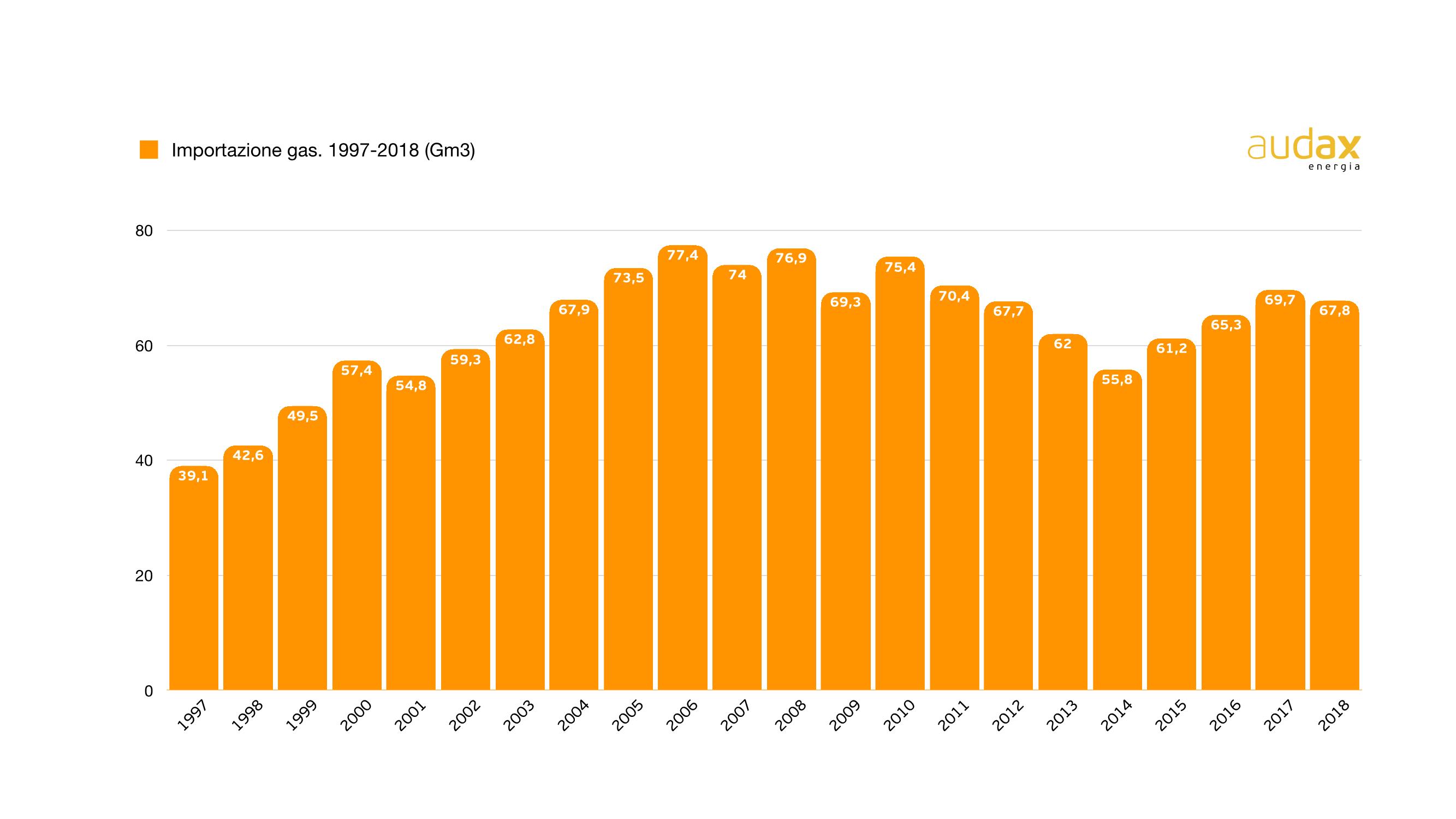

And Italy's energy dependence on other states does not spare - as can be imagined - even natural and liquefied gas. In 2018, in fact, 67 billion cubic meters of gas were imported, with a decrease of 2.6 billion compared to 2017.

Arrived almost entirely via pipeline (over 90%), the gas used in Italy is for the 44% of Russian origin (with 29.5 billion cubic meters); followed by the Algerian one (25%), with 17.1 billion cubic meters - but rather reduced after the exploit of 2016 - the one from Northern Europe (Norway and Holland) and the one coming from Libya. However, if the import from Northern European countries shows a positive sign (+7% in 2018) the Libyan one, also due to the internal difficulties of the African nation, continues to decrease (4.4 billion cubic meters).

With the Trans Adriatic Pipeline (TAP) coming into operation, expected in 2020, the quotas could change and help lower the cost of gas for Italian consumers. In Italy, end customers pay on average 10% more for gas than in Northern European countries.

The expected transport capacity will be approximately 10 billion cubic meters, with the possibility of satisfying the needs of 7 million families.

LNG continues to grow, representing 7% of imported gas to date.

Chart 1. Gas imports. 1997-2018 (Gm3)

Source: ARERA on MISE DGSaie data

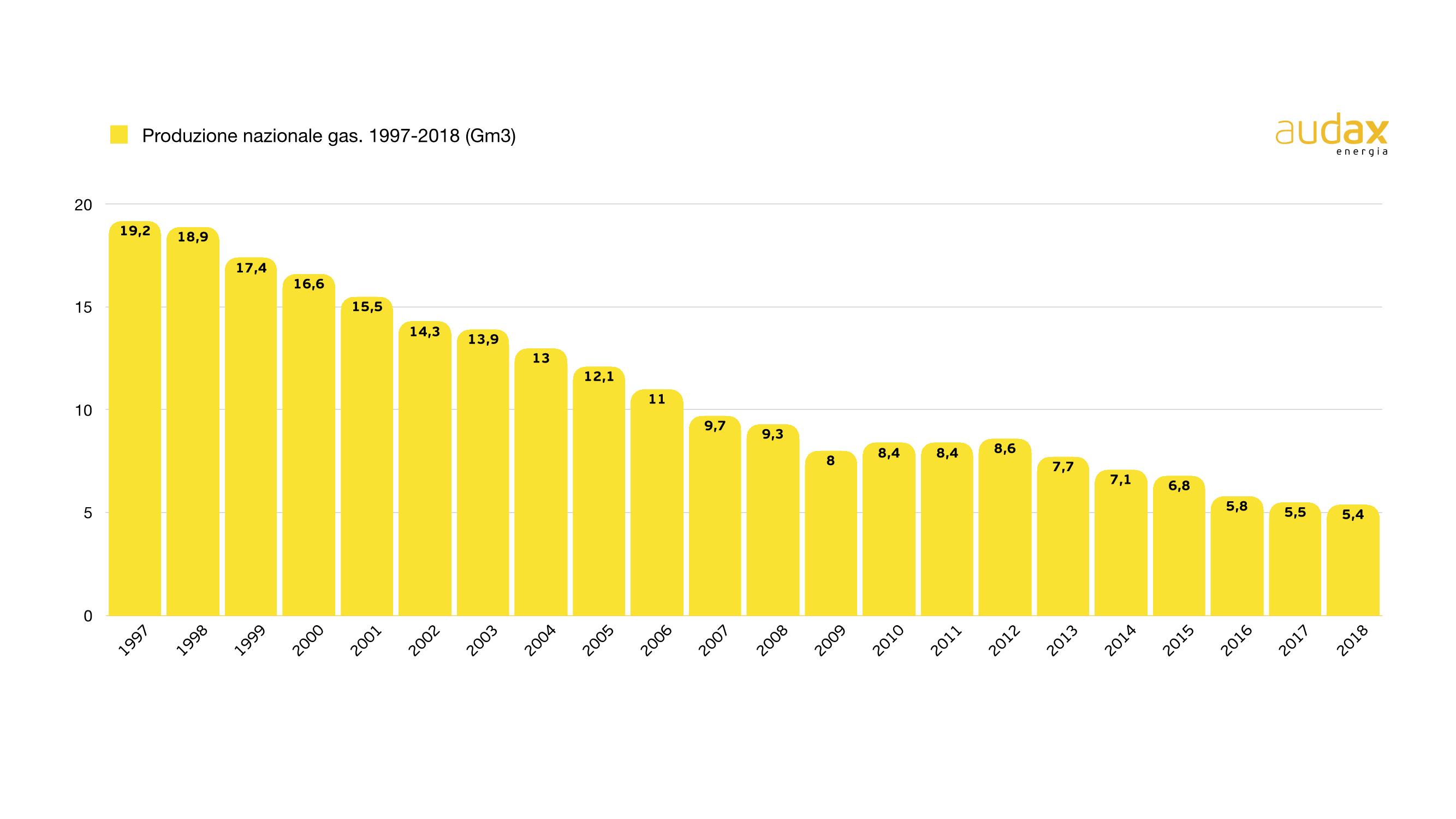

And what about domestic production? After years, 2018 showed a less significant decline than in the past (-1.6%); in the space of 10 years, however, Italian production halved, going from 9.3 billion cubic meters in 2008 to just over 5.4 billion last year.

Graph 2. National gas production. 1997-2018 (Gm3)

Source: ARERA on MISE DGSaie data

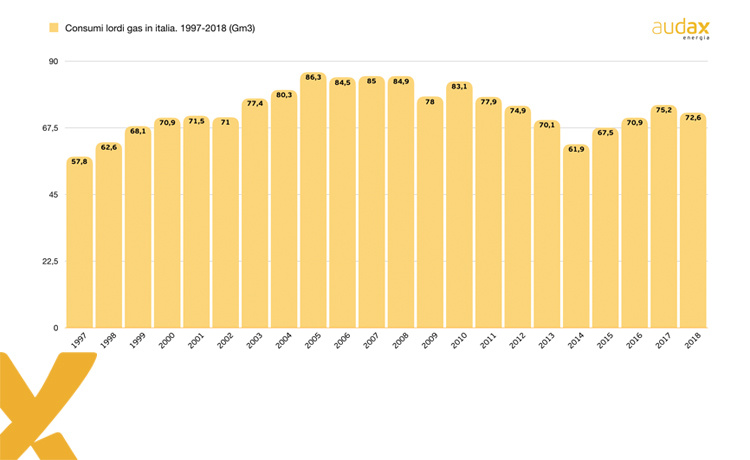

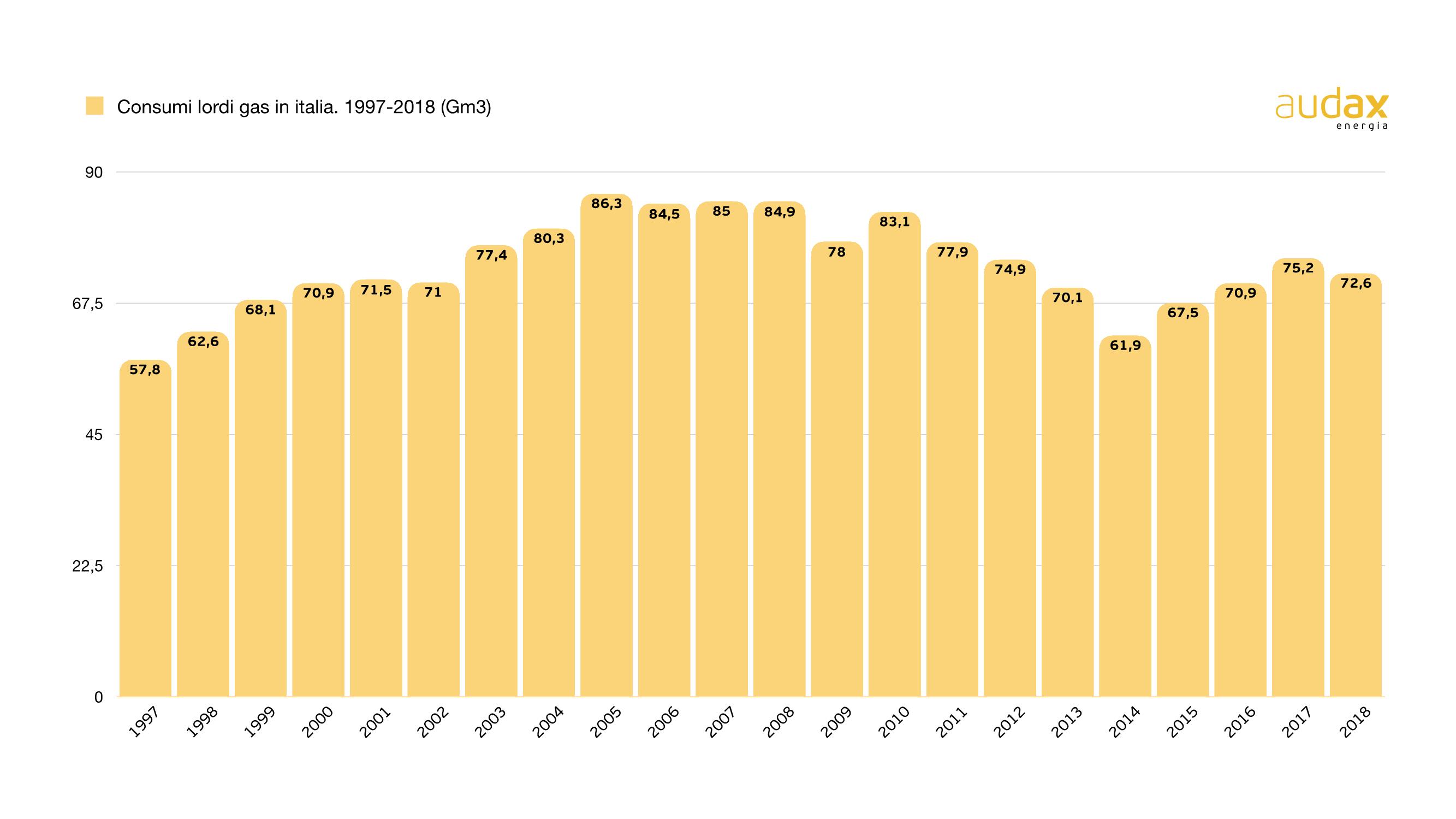

Consumption reached 72.6 billion cubic meters in 2018, a decrease of 3.3% compared to the previous year. The cause of the decrease was the lower demand for thermoelectric energy, the gas used to produce electricity. A decrease of 7.6% due essentially to three factors such as: a greater contribution from renewables, more energy from hydroelectricity, more nuclear purchased in France.

In any case, consumption levels are still below those of 2003, when over 86 billion cubic meters were consumed (source MiSE-DGSAIE)

Gross gas consumption in Italy. 1997-2018 (Gm3)

Source: ARERA on MISE DGSaie data

Without overshadowing the role played by its big brother – oil – gas has become an important strategic lever to be used in political and economic relations between states. Indicated as the fuel of the energy transition, it has become – for some time now – a sensitive thermometer of the geopolitical situation. And it is evidently conditioned by this. But not only that, elements such as climatic conditions – for example cold winters or springs that are slow to appear – can negatively affect the price.

In any case, the “macro” conditions the “micro”, which means repercussions on prices not only at wholesale, but also on the bill. The Energy Observatory of the Facile.it portal, analyzing over 63 thousand contracts collected during 2018, estimated that if electricity weighed 417 euros/year on the expenditure of an average Italian family, gas came to impact for a good 762 euros.

From a prospective point of view, the outlooks of international organizations (such as IEA) or the study centers of large groups (such as BP) try to estimate the price trend in the coming years. The forecasts speak of a long-term increase in the cost of natural gas in Asia, thanks to the increase in demand, anti-pollution policies and the construction of new transport infrastructures. At the same time, in Europe there will be strong pressure on prices due - in addition to the choices of CO2 mitigation - to competition between European and Asian consumers.

In all this, future scenarios show a global demand for natural gas increasing by 46%, at least until 2040. Also following a progressive reduction in the shares currently occupied by oil (from 32% to 29% by 2040) and coal (from 27% to 21%).

Finally, a look at China alone. The Asian country represents 37% of the global increase in natural gas consumption between 2017 and 2023: no one more than Beijing. The growing need will make it the largest natural gas importing nation in the world by this year and, with 171 billion cubic meters by 2023, one of the most served by LNG. The driving sector will be industry, responsible for over 40% of the increase in natural gas consumption.

Sources:

- ARERA, Statistics data

- Gas Exporting Countries Forum (GECF), 2018 Global Gas Outlook Synopsis

- International Energy Agency (IEA), GAS 2018. Analysis and Forecast to 2013 (executive summary)

- BP, Energy Outlook 2019